IAS 38 Intangible Assets in Financial Reporting/F7

IAS-38: Intangible Assets

Introduction:

International Accounting Standards (IAS) provide proper guidance for accountants to follow globally. They outline all the principles and accounting concepts to avoid any confusion and subjectivity in reporting for accountants around the world.

Introduction to IAS 38 Intangible Assets

One of the major accounting standards is IAS 38: Intangible Assets. This standard outlines the accounting requirements for all intangible assets. An intangible asset is a non-monetary asset that doesn’t have a physical substance.

For example:

Goodwill

Trademarks

Computer Softwares

Trade License

Customer List

Patents

Databases

Marketing Rights

Royalties

How to Identify an Intangible Asset?

An intangible asset cannot be physically seen, so recognizing such assets is based on some conditions or criteria.

First of all, it should have a reliable cost that can be taken into account. Without a reliable value, it cannot be measured or even recorded in accounting books. Secondly, there has to be reasonable evidence to support the life of the given asset. It must be ensured, that the asset is going to exist for the given timeline. Thirdly, the role of the asset must be clear in terms of the future economic benefit to be achieved. Also, the dynamics of the probable economic benefit gained from an intangible asset will also help with its initial valuation. If an asset fails to be recognized as an intangible asset, then it must be taken into account as an expense incurred.

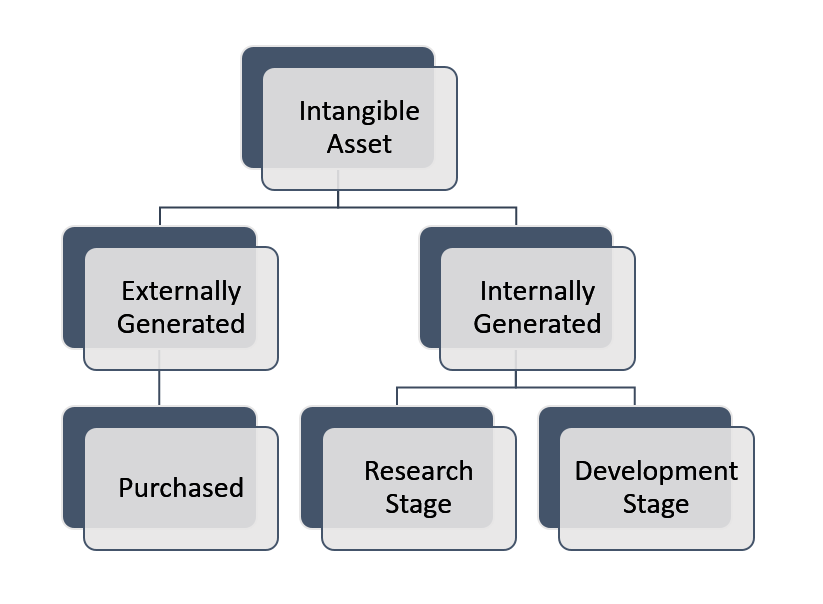

Categories of IAS 38 Intangible Assets

There are two categories of intangible assets:

Externally Generated

is

Purchased Intangible Asset: A purchased intangible asset is one which is acquired externally in exchange for cash or cash equivalents. It is identified separately from the entity. For example, company A buys company B and pays PKR 100 million for the acquisition. The accumulated value for all assets and liabilities makes up to PKR 90 Million, so the 10 million extra payment was for the goodwill of Company B, which will come along with the acquisition. This way, Company A has purchased an intangible asset of Company B. There can be various other intangible assets that can be purchased, such as licenses, internet domains, import quotas, etc.

Internally Generated

Internally generated intangible assets are those that a company creates itself, such as computer software. However, its accounting is in two stages:

Research Stage:

This is a very initial stage when there’s a fresh plan for the investigation to obtain new knowledge. The intangible assets are under work-in-progress at this level. At this stage, the company is exploring and examining the results and usefulness of the asset that they are planning to obtain. This stage is too early to gain any economic benefit; hence, it cannot be capitalized. As it is not currently identified as an intangible asset so all the expenditures done on the research and creation for it till now must be expensed into income statement immediately, these will reflect as revenue expenditures in the period they are incurred.

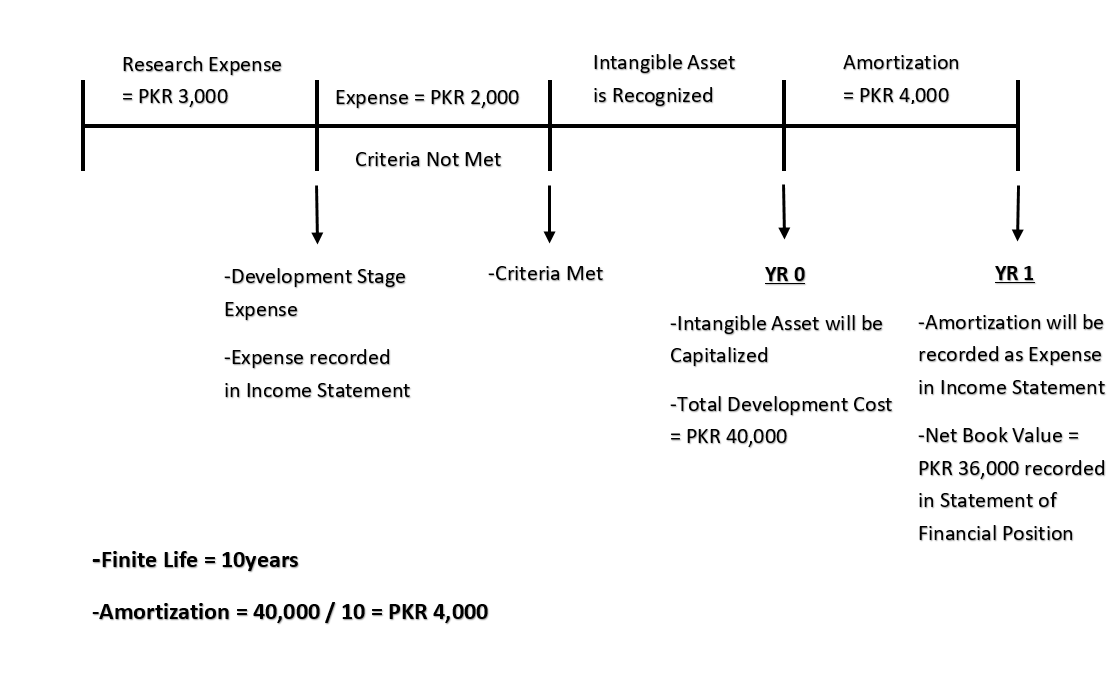

Development Stage:

This is the stage when intangible assets have taken their final form. All the knowledge obtained can now be applied and be of use to the company. Now it can be capitalized, however, following a “PIRATE” criteria. This criterion is based on 6 conditions an asset needs to fulfill before it is capitalized.

P = Probable chances of economic benefit (there have to be certainty on the oncoming of returns and gains in the short and long run from this asset)

I = Intention to complete (the company has to complete the creation of this asset, if not already done)

R = Resource availability (there must be sufficient human and financial resources for the completion and usage of the given asset)

A = Ability to use or sell (a company should be able to use the asset, they must know or have plan as for when, where and how to use the asset obtained)

T = Technical knowledge available (intangible assets such as computer software or patented technology require technical knowledge in order to be used, the availability of which is highly necessary)

E = Expenditure reliably measured (there must be an evidently reliable measure of all the expenses and costs that went it it’s development, without it the asset can not be valued and accounted)

These 6 conditions must be fulfilled in order to capitalize the expenditure. Absence of even one of these will result in development cost being expensed in income statement.

Subsequent Accounting for Intangible Assets

Like all other Non-Current Assets, intangible assets are also recorded according to 2 costing models in Financial Statements:

Cost Model

As per the cost model, the value of the asset is booked at initial cost, Whether it be purchasing cost or development cost capitalized. Then these Assets are amortized over their useful life. Amortization is similar to depreciation, each year intangible assets are amortized (depreciates). To calculate amortization its initial cost is divided by its finite life.

Amortization = Capitalized Dev. Cost / Finite Life

Amortization expense is recorded as expense in Income Statement and it is deducted from cost to make Net Book Value of the Asset in Statement of Financial Position. Besides this, intangible assets are also subject to impairment loss which is also deducted from cost similarly. Impairment is a sudden fall in carrying value of assets due to any given external or internal factor. Assets must be subject to impairment testing given a certain periodan. roomIf impairment loss is realized at the end of the accounting period, similar to amortization, it will also be recorded as an expense in the Income Statement and deducted from the rom cost for NBV in Statement of Financial position.

Revaluation Model

According to the revaluation model, intangible assets are revalued in the same way as tangible assets. Assets are recorded at their initial value, and after every accounting period, this value is compared to its market value. When the market value is greater than carrying amount, it shows a surplus. This surplus is recorded in the Statement of Comprehensive Income as Revaluation gain. A limitation to this model is that it can only be used if the fair value of the asset can be determined in reference with an active market. In the real world, an active market may not be available or common for such assets because of the unique nature of some of the intangible assets. An active market is one where there is frequent trading of the given asset.

Finite Life:

In the case of intangible assets with a finite life, it’s not a compulsory annual impairment test; however, there will be hints or indications there.

Indefinite Life:

In the case of intangible assets that have an indefinite life, amortization won’t be done, but an annual impairment test must be done.

Timeline for intangible asset capitalization for reference:

This article explains the accounting treatment for research and development (R&D) costs under both UK and International Accounting Standards. Both UK and International Accounting Standards recognise the importance of accounting for R&D, but take a different viewpoint as to the method used – Read more

FAQs (Frequently Asked Questions)

1). What are IAS 38 intangible assets?

The standards for identifying and quantifying intangible assets are outlined in IAS 38, which also mandates disclosures regarding them. An identified non-monetary product lacking physical substance is called an intangible asset. When an asset can be divided into different categories or when it derives from a contract or other legal right, it can be identified.

2). What are examples of identifiable intangible assets?

Intellectual property involving patents, trademarks, and copyrights, as well as non-cash government awards like broadcasting licenses and airport landing rights, are examples of identifiable intangible assets. Identifiable intangible assets usually stay with a corporation for the duration of its existence, making them indefinite.

3). What does IAS 36 say?

If the carrying amount of an asset is greater than the amount that can be recovered through the use or sale of the asset, the asset is carried at more than its recoverable amount. In such a scenario, the asset is considered impaired, and the company must recognize an impairment loss in accordance with the standard.

4). What is IAS 36 in IFRS?

The basic principle of IAS 36 is that an asset cannot be valued higher in the financial statements than the maximum amount that can be obtained from its sale or usage. The asset is deemed impaired if the carrying amount is higher than the recoverable value.

Q5). Can internally generated goodwill be capitalized?

No, it cannot be capitalized.

Q6) Does impairment loss come in both revaluation and cost models?

Yes, any indication of impairment can arise in either accounting model.

Q7) What are a few examples of intangible assets with infinite life?

Taxicab licenses, trademarks, and broadcasting rights are a few examples of intangible assets with infinite life until there is any indication of impairment.

Q8). When does a company start to amortize its intangible assets?

An intangible asset starts to amortize once it is ready to use, so the amortized expense matches the economic benefit taken from it over the given period.

-Written by: Mohammad Anas Khamisa Student at Mirchawala’s Hub of Accountancy

How Many ACCA Modules Are There? Expert Insights

How to Get ACCA Practising Certificate in Zimbabwe: A Complete Guide

Emerging Skills for ACCA Professionals in Zimbabwe

Why Pursuing ACCA in the Middle East is a Smart Career Move

Best ACCA Institutes in Faisalabad

… [Trackback]

[…] Information on that Topic: mirchawala.com/ias-38-intangible-assets/ […]

… [Trackback]

[…] Information to that Topic: mirchawala.com/ias-38-intangible-assets/ […]

… [Trackback]

[…] Info to that Topic: mirchawala.com/ias-38-intangible-assets/ […]

… [Trackback]

[…] Read More to that Topic: mirchawala.com/ias-38-intangible-assets/ […]

Comments are closed.